The Global Economy Is Forecast to Post ‘Sturdy’ Growth of 2.8% in 2026

预计全球经济在2026年有2.8%的强劲增长

Goldman Sachs Research’s forecasts for growth in most major economies in 2026 are at or above consensus estimates. It is most optimistic (relative to consensus) about the US because of tax cuts, easier financial conditions, and reduced drag from tariffs.

高盛对世界主要经济体在2026年的预测等于或者高于市场的共识估计。最为乐观的是美国(相对共识而言),因为减税,更宽松的金融环境,关税负担的减轻

In China, our economists expect robust growth in manufacturing but continued weakness in parts of the domestic economy.

对于中国,我们的经济学家预计制造业会强劲增长但是国内部分经济持续疲软

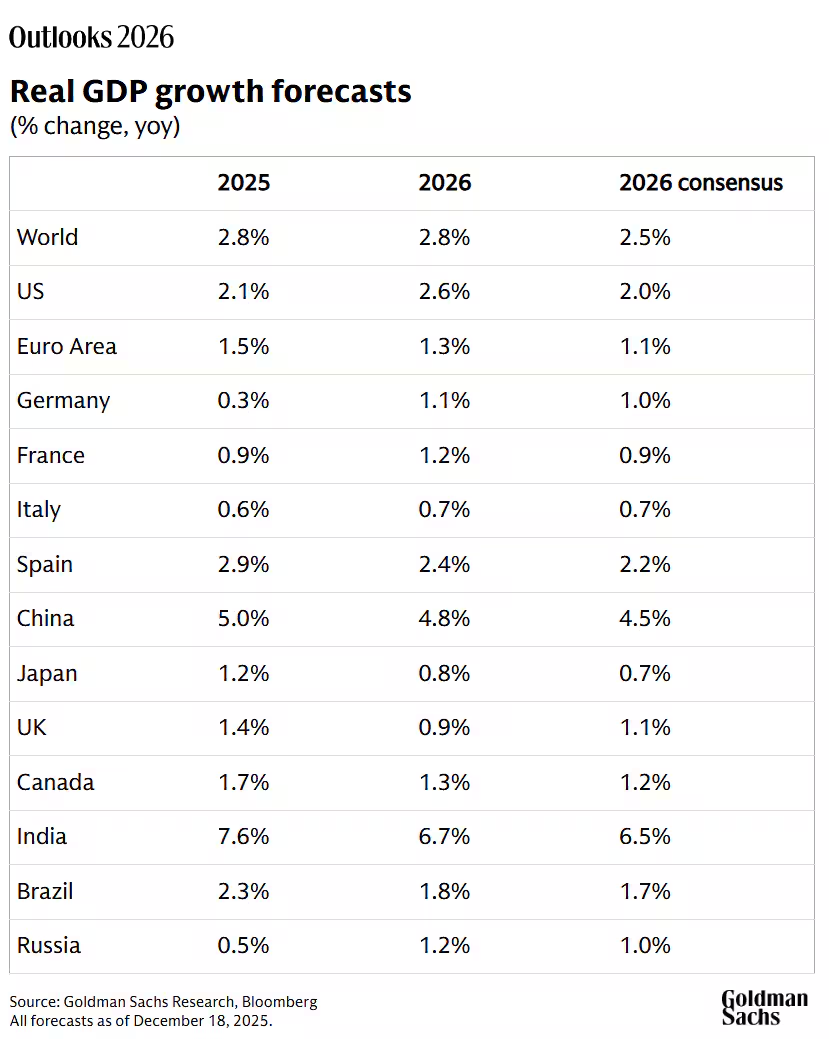

Despite longer-term challenges and competition from China, the euro area economy is forecast to increase 1.3% next year, owing to fiscal stimulus in Germany and strong growth in Spain.

尽管长期收到来自中国的挑战和竞争,在接下来的一年,欧元区被预测会有1.3%的经济增长,得益于德国的财政刺激和西班牙的强势增长

Our economists expect core inflation to moderate and policy rates to decline in developed markets in 2026.

我们的经济学家预计2026发达国家的核心通胀趋于温和政策利率会下降

The global economy is forecast to generate “sturdy” growth in 2026, according to Goldman Sachs Research. In fact, our economists’ projections for most major countries are at or above consensus estimates.

What is the global economic outlook for 2026?

Global GDP is projected by Goldman Sachs Research to increase 2.8% in 2026 (versus the consensus forecast of 2.5%). US econemic growth is expected to accelerate to 2.6%, while China’s GDP expands 4.8% as strong exports outweigh sluggish domestic demand. Despite longer-term challenges, our economists predict the euro area economy will increase 1.3%, owing to fiscal stimulus in Germany and strong growth in Spain.

“As has typically been the case since the pandemic, we are most optimistic (relative to consensus) in the US,” writes Jan Hatzius, chief economist and head of Goldman Sachs Research, in the team’s report titled “Macro Outlook 2026: Sturdy Growth, Stagnant Jobs, Stable Prices.”

在《2026年宏观前景:强劲增长、就业停滞、价格稳定》的报告中Jan Hatzius提出,正如疫情之后的典型情况一样,我们对美国最乐观(相对于共识)

What is the forecast for US GDP growth in 2026?

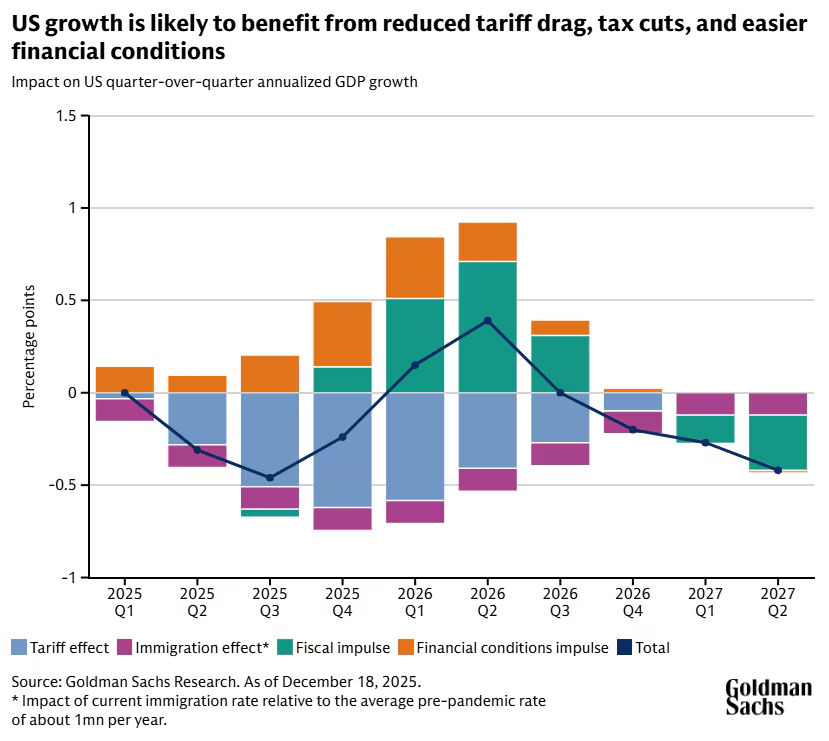

The US is expected to substantially outperform consensus estimates because of tax cuts, easier financial conditions, and a reduced drag on the economy from tariffs. As a result of tax cuts, for example, consumers will receive around an extra $100 billion (0.4% of annual disposable income) in tax refunds in the first half of next year.

因为减速,更宽松的金融环境,关税负担的减弱,美国的表现将大大超过共识估计。拿减税来举例,消费者将会在明年的上半年收到额外的1000亿美元的退税(每年可支配收入的0.4%)

The impulse from these forces is expected to be front-loaded in the first half of 2026, and the rebound from the US government shutdown will also provide a boost. “We expect especially strong GDP growth in the first half of next year,” Hatzius writes.

这些因素带来的推动力预计将在2026年上半年集中释放,同时美国政府关门后的复苏也将提供助力

Hatzius写到我们预计上半年GDP将会有强劲的增长。

However, while global GDP is rising, it hasn’t resulted in stronger performance from the labor market. Job growth across all major developed-market economies has now fallen well below the rates prevailing in 2019, just prior to the pandemic.

然而,尽管全球GDP在增长,但劳动力市场的表现并未随之增强。目前,所有主要发达市场经济体的就业增长已大幅低于疫情前2019年的水平

Although it doesn’t provide the full explanation, the job-market weakness mirrors the sharp downturn in immigration and, in turn, labor force growth, Hatzius writes. The disconnect in employment is most pronounced in the US, where job growth may well have been negative over the summer.

Hatzius指出尽管这一因素无法完全解释现状,但就业市场的疲软反映了移民的急剧减少,进而导致劳动力增长放缓。就业市场的脱节在美国最为明显,夏季期间的就业增长很可能已转为负值(到底是移民效应导致的就业疲软还是自动化替代?)

The impact of artificial intelligence (AI) on jobs and productivity, meanwhile, has so far mainly been confined to the technology sector, according to Goldman Sachs Research. Our economists expect that the largest productivity benefits from AI are still a few years off.

与此同时,高盛研究部指出,人工智能(AI)对就业和生产力的影响目前仍主要局限于科技行业。我们的经济学家预计,AI带来的最大生产力提升仍需几年时间才能显现。

The outlook for China’s economy in 2026

The narrative for China’s economy is much more mixed. China’s ability to produce increasingly higher quality goods at lower prices remains unmatched, Hatzius writes. The world’s second-largest economy has demonstrated that it has the capability to deter high tariffs on its exports, as seen in recent trade negotiations with the US.

Hatzius:“中国经济的情况更为复杂。中国以更低价格生产质量不断提升的商品的能力仍无可比拟。作为全球第二大经济体,中国已展现出阻止出口商品遭遇高关税的能力,这一点在最近的美中贸易谈判中可见一斑。”

“All this suggests that the Chinese manufacturing sector should continue to grow robustly,” Hatzius writes.

At the same time, large parts of China’s domestic economy remain weak. While the largest drag on GDP growth from the property downturn has probably already taken place (property sales are down 60% and property starts are down 80% from the peak), our economists estimate that the property sector will produce a 1.5 percentage point drag on GDP growth next year.

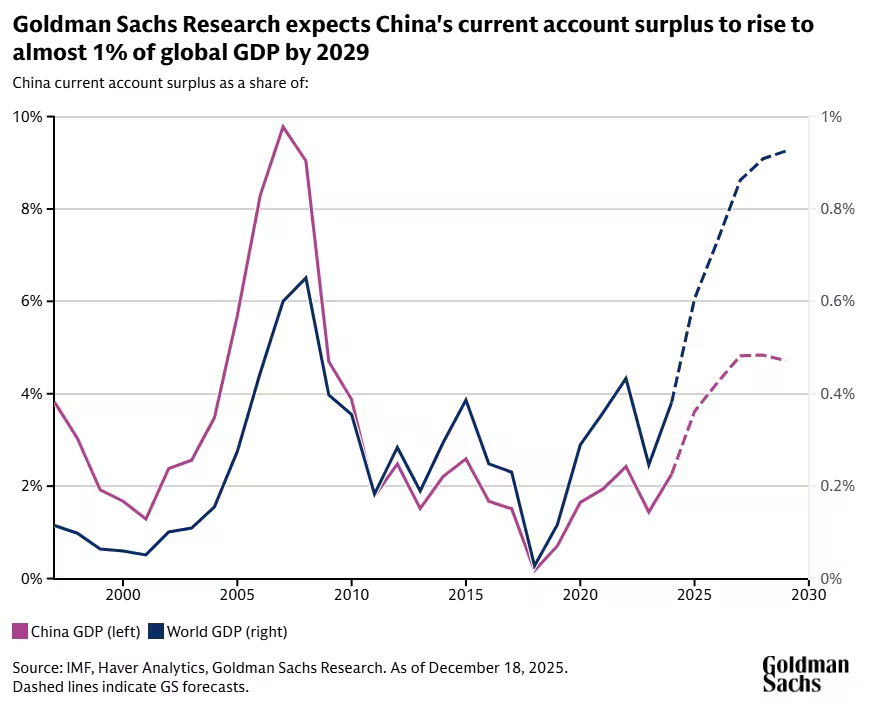

“The combination of a strong manufacturing sector and weak domestic demand is pushing China’s current account surplus ever higher,” Hatzius writes.

Our economists expect its current account surplus to increase to almost 1% of global GDP over the next 3-5 years, the biggest surplus of any country in recorded history. “This is likely to weigh heavily on growth in economies that compete intensively with China such as the euro area, and particularly Germany,” Hatzius adds.

我们的经济学家预计,未来3至5年,中国的经常账户盈余将增长至全球GDP的近1%,成为有记录以来任何国家中规模最大的顺差。Hatzius:“这种局面可能会对与中国经济竞争激烈的国家(如欧元区,尤其是德国)的增长前景构成沉重压力

What is the forecast for the euro area’s economy in 2026?

Increased competition from China reinforces the structural weaknesses of the euro area economy, including demographic decline, overregulation, and high energy costs, according to Goldman Sachs Research.

高盛研究指出,来自中国的竞争加剧了欧元区经济的结构性弱点,包括人口下降、过度监管以及高昂的能源成本

Despite these challenges, the euro area should grow at a “decent” 1.3% pace in 2026, Hatzius writes. GDP growth in Germany is expected to benefit from the sharp increase in federal government spending that is underway. And our economists expect growth in Southern Europe to remain solid, especially in Spain where real consumer spending has continued to grow at around 3% and the economy’s diversification into higher value-added services continues apace.

Hatzius:尽管面临这些挑战,欧元区在2026年的经济增长率仍有望达到稳健的1.3%。德国的GDP增长将受益于当前正在进行的联邦政府支出大幅增加。我们的经济学家预计,南欧地区的经济增长将保持强劲,尤其是西班牙,其实际消费支出持续以约3%的速度增长,且经济正持续推进向高附加值服务业的多元化转型

Inflation is forecast to moderate in 2026

Core inflation in developed markets is expected to fall to levels that are broadly consistent with policy targets in 2026.

In the US, the main reason why core Personal Consumption Expenditures (PCE) inflation has remained elevated in 2025 is because of tariff pass-through. Excluding tariffs, our economists estimate that inflation has continued to fall and now stands at 2.3%. And although tariff pass-through will likely rise modestly further (assuming tariffs stay around their current levels), the impact on year-on-year inflation will diminish sharply in the second half of 2026 because of favorable so-called base effects.

在2025年,美国核心个人消费支出(PCE)通胀率居高不下的主要原因在于关税传导效应。剔除关税因素后,我们的经济学家测算通胀率持续回落,目前已降至2.3%。尽管关税传导效应可能会小幅上升(假设关税保持在当前水平),但由于基数效应的有利影响,其对2026年下半年同比通胀率的冲击将显著减弱

An important factor weighing on inflation in the US and UK is the notable recent slowdown in wage growth in both economies. In the US, nominal wages are now growing below the 4% “sustainable” rate that our economists estimate is consistent with 2% inflation. In the UK, the most recent pace of wage growth is close to our economists’ estimate of the sustainable rate of 3%.

美国和英国通胀受到抑制的一个重要因素是两国近期工资增长的显著放缓。在美国,名义工资增速目前已低于我们经济学家估算的4%“可持续水平”——这一水平与2%的通胀目标相一致。在英国,最新工资增速已接近我们经济学家估算的3%可持续水平

What is the outlook for central bank rate cuts in 2026?

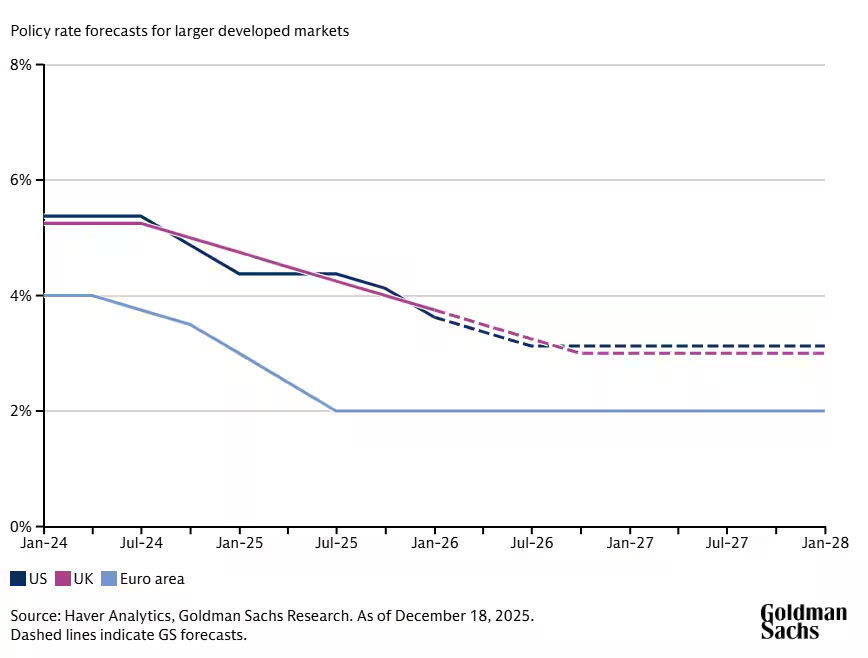

As with inflation, Goldman Sachs Research expects developed-market policy rates to converge lower in 2026. Three of the countries with higher policy rates—the US, UK, and Norway—are forecast to make further cuts.

The US Federal Reserve is projected to reduce its policy rate by 50 basis points to 3-3.25% in 2026. Goldman Sachs Research’s view is that the US inflation issue has been resolved, and there’s potential for the Fed to cut rates more than expected.

Our economists’ baseline forecast for the UK is a sequence of quarterly rate cuts to 3% by the third quarter of 2026. Meanwhile Norway’s central bank is expected to cut rates by 50 basis points to 3.5% in 2026. The European Central Bank, by contrast, is expected to hold policy rates steady as inflation falls.